Why startups and media broadcasters in the emerging Europe region should look at this opportunity

Media for growth investments are increasingly being acknowledged as powerful engines for sustainable growth. Such investments play an important role in revenue diversification for media broadcasters, whilst startups benefit from customer growth, increased brand awareness, and guidance from media groups, all without having to spend cash.

Today, there are more than 30 specialised funds offering advertising and media services in exchange for equity. In the last two decades, over 1,000 startups raised media for growth funding including Zalando, AboutYou, Carwow, Pinterest, and Glovo. And yet the Central and Eastern Europe region is lagging behind.

—

The media for growth business model is approximately 30 years old. Europe is considered the birthplace of media for growth with funds such as Seven Ventures (ProSieben1) and German Media Pool in Germany and Aggregate Media in Sweden being among the originators of this investment model.

As the model proved to be successful, other media groups started trading advertising in exchange for equity in France (5M), the UK (Channel4Ventures, ITV AdVentures, UKTV Ventures), Italy, and Spain (Ad4Ventures), Sweden/Finland (8mediaventures).

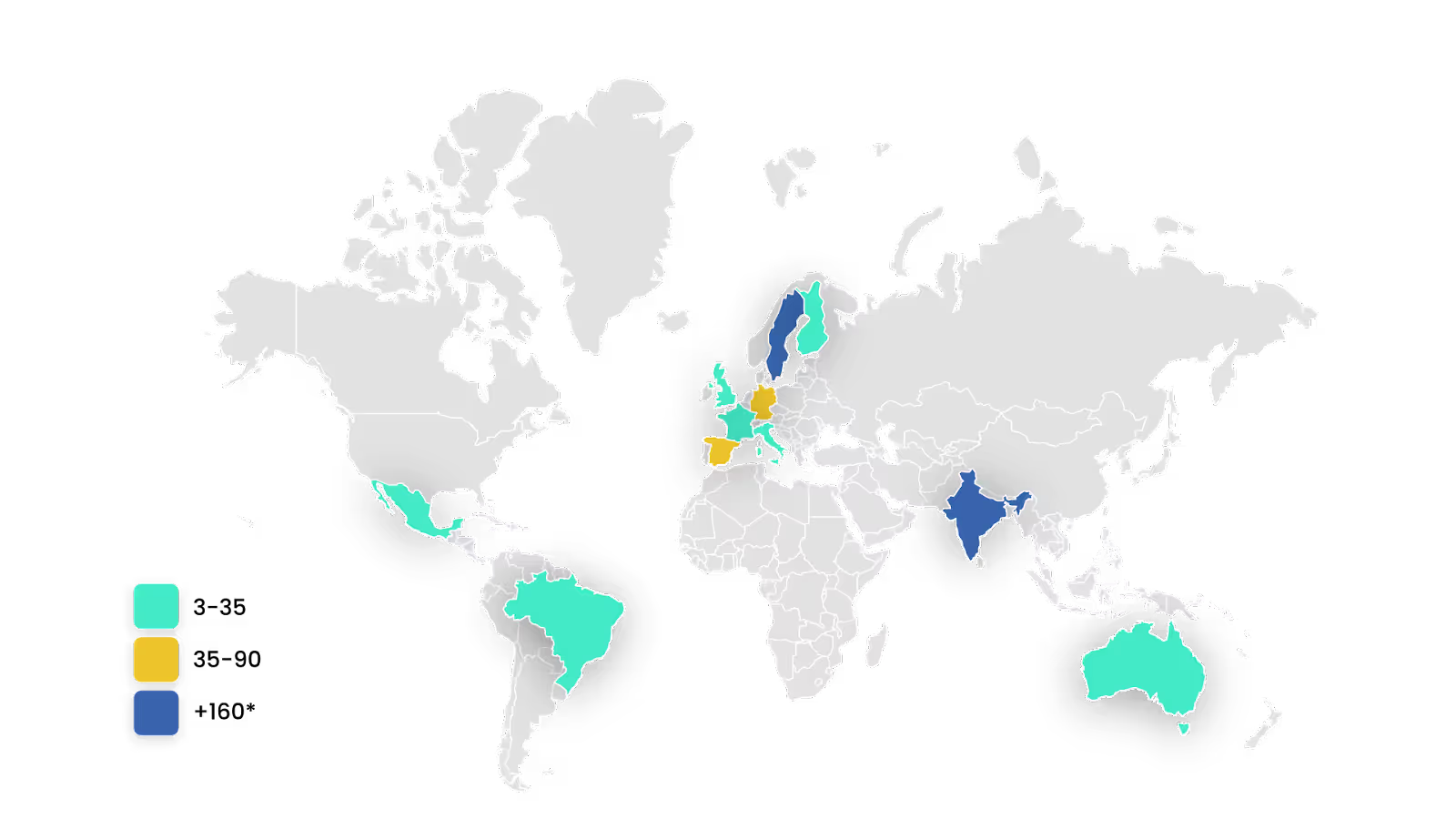

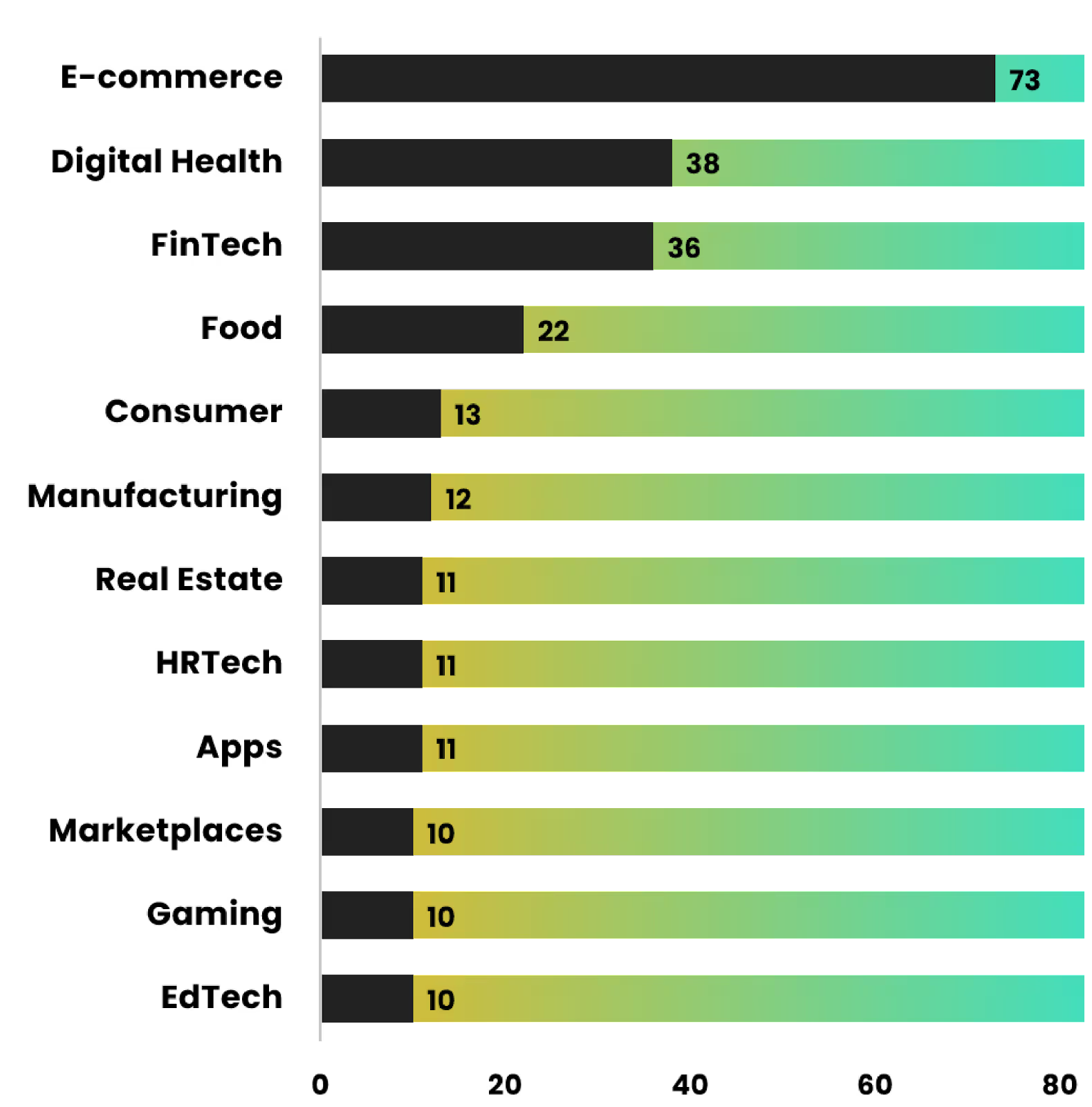

Leading European countries by no. of investments include Sweden (167), Germany (90), Spain (35), and the UK (30) according to the latest research conducted by mediaforgrowth, the first dedicated network of media for growth funds representing this ecosystem.

The mediaforgrowth team could only confirm that TVN - one of Poland’s largest media networks has completed at least one such investment prior to 2016 when the group was acquired by Discovery.

Media for growth funding was also raised in France (10), Italy (5), and Finland (3). In India, the Times Group completed 900+ investments. In LATAM, Televisa is one of the most active investors with 11 deals completed to date. There have been five investments registered in Brazil. Australia registers nine investments whilst in North America there is only data available on three investments completed by Arrandale Ventures (and consumed in North America).

So what’s holding the region back?

#1 Media landscape

- TV rules the CEE ad market. In countries such as Romania, Poland, Bulgaria or Croatia the share of people watching TV on a TV set every day exceeds 80%. Most TV stations do not struggle to fill up inventory, in fact in some markets such as Romania, TV inventory is saturated allowing media broadcasters to charge a premium. This is an important aspect when considering how media for growth funding started in the late 90s.

Some of the first major deals were realised in Germany by ProSiebenSat.1 Media, which at the beginning followed the unsold inventory strategy. They saw an opportunity in diversifying their revenue streams.

An independent media for growth fund may be better suited to meet current market conditions in CEE. Unlike the “corporate”-backed funds owned by media groups, such funds have partnership arrangements with a set of media companies, often covering different media types. Due to the number of partners and media types, this approach is more challenging to set up and manage but can provide startups with a greater range of media options. Founded in 2002, Aggregate Media in Sweden is the inventor of this innovative MFG model.

#2 Startups business model

- Media for growth funding favors certain types of businesses and industries. According to our study, 70% of the startups that raised media for growth funding operate on a B2C model. Among the most popular industries are e-commerce, digital health, fintech, food, and beverage.

In a market where capital has been scarce, CEE founders have been focussing on high-growth, low capex, scalable business models (B2B SaaS) targeting 7-8 years exits to attract VC funding. The region’s particular strength lies in enterprise software which attracts twice the share of VC funding that the rest of Europe. Out of the 34 unicorns that have been created in CEE to date, only 8 (24%) operate on a B2C model.

Consumer brands have longer time horizons and don't fit the time horizons of VC fund lifecycles typically. Founders in this domain need to think about playing the long game and building enduring businesses that are built to last. Lululemon took 24 years to its valuation today. It was founded 1 year after Google which is now a trillion $ company. Most consumer brands such as Cadburys, Hermes, and Nike have been around for over 100 years, whilst VCs want returns in 7-10 years.

If accessible, media for growth funding could encourage more founders to build consumer businesses knowing they can tap into more diversified investment options. Some of the benefits of raising media for growth funding include:

- Extending your startup runway by preserving cash and optimising spending across marketing channels.

- Being accompanied by an experienced team that understands both worlds, the online performance approach, and the offline branding approach. Some investors such as Channel4Ventures in the UK or The Times Group of India also provide creative support.

- It allows you to raise larger financing rounds, focusing part of the capital on building long-term value. According to our research media for growth-backed startups raise on average 3x more funding than other startups before they got acquired. On average these companies raised $83 million pre-acquisition.

#3 Broadcasters' readiness to innovate

To innovate corporations have used different tools at their disposal from R&D and M&A to working with startups to form strategic partnerships. Media for growth funding should be understood as a way to diversify their revenue stream and is not a lot different from the traditional CVC model which only started gaining more prominence in CEE in the last decade.

The biggest challenge with enabling airtime in exchange for equity is balancing business-as-usual (BAU). TV advertising is measured on KPIs and short-term financial targets – a CEO of a TV station or a TV show producer would always prioritise cash over outputs they cannot see. Squaring this requires a fundamental shift in the way media holdings are designed.

A potential solution is to start at the top – where the C-suite looks after the core business and the investment unit is governed separately.

Taking a collaborative approach may maximise the chances of returns, faster. Take ProSieben.1’s SevenVentures and German Media Pool, which together made a €39 million media for growth investment in FRIDAY, a leading German digital insurer. SevenVentures provided significant media exposure across its TV assets, whilst German Media Pool complemented the deal through radio, out-of-home, print, and other television properties.

German Media Pool boasts a 57% exit rate among its portfolio of 38 companies. The most popular combinations of two media types were television with radio (5 companies) and television with out-of-home (5 companies).

—-----

The State of Media for Growth funding white-paper is available to download here.

If you’re running a high-growth (post-revenue) digital startup, you can apply to learn more about media for growth funding and to get connected with the decision-makers at MFG. Please fill out the form HERE.

About mediaforgrowth

mediaforgrowth is the first global network to align the interests of startups, investors, and experienced media professionals. First, they partner with later-stage founders to grow revenue and scale internationally using media for growth investments. Secondly, they connect emerging and established media for growth funds with investors around the world to optimise the startup investment process. mediaforgrowth members include some of the world’s largest media groups such as The Times Group, 30+ media for growth funds, individual investors, early-stage VCs, and equity investment platforms.

Methodology & Data Limitation

The insights shared in this report have been gathered through publicly available data sources and semi-structured interviews with startup founders, investors, and media for growth funds. We aggregated data from media for growth funds formed more than five years ago as well as publicly and privately available datasets. Overall we analysed the data of 382 unique investments completed during or after 2000.

.avif)

.avif)